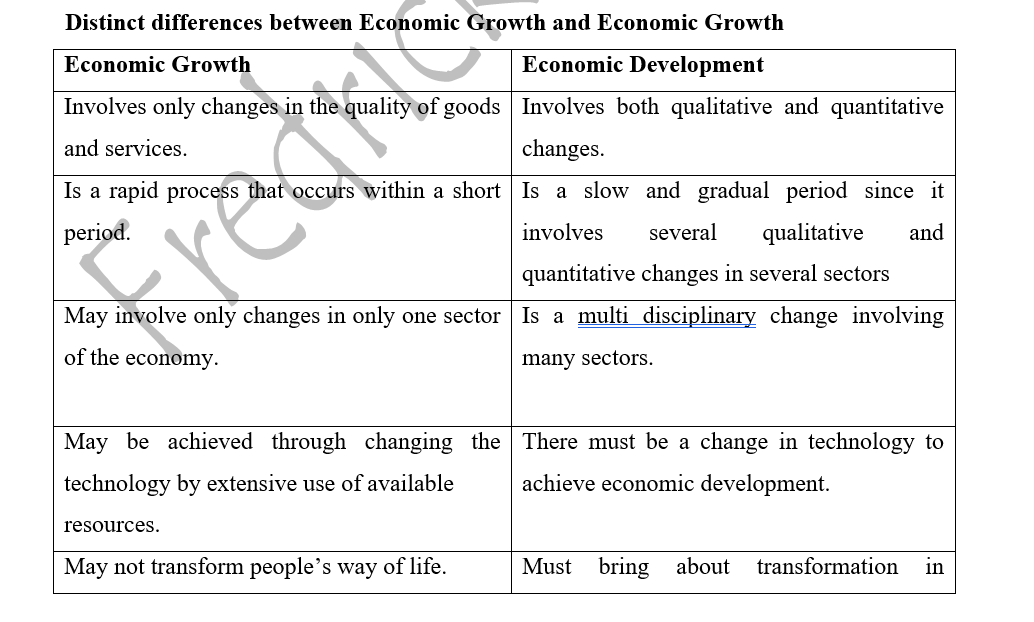

Economic growth –Refers to the changes (increases/decreases) in the level of output (amount of goods and services) produced in an economy within a period of one year i.e. It is an increase/decrease in real Gross Domestic Product (GDP) and real per capita income in a nation over a given period. Thus it is a quantitative change in the volume of goods and services produced and the production capacity of a country over a given period of time.

N/B: An increase would be realized when the demand of amount of goods and services in a particular country increases more steadily than the number of population growth and vice versa.

Economic Development –Refers to a multi-dimensional process of transformation/change involving accumulated qualitative and quantitative changes in an economy leading to better standards of living, cultural changes, economic transformation, education reforms, and political revolutions e.t.c. It is a continuous process covering a long period; economic development involves economic growth which eventually leads to change in people’s way of life, fairer distribution of wealth and provision of essential goods and services thus improvement of living standards.

Characteristics of a Developing nation

- Low standards of living – most LDCs are characterized by low standards of living as noted by poor nutrition, medical care, sanitary services, poor transport and education e.t.c.

- Low levels of income

Low income leading to low purchasing power and limited market, it is because much of labour force is engaged in agriculture which is the dominant sector.

- Pre-dominance of peasant agriculture

Majority of the populations are engaged in agriculture which is the dominant sector.

Agriculture is unproductive since primitive tools and methods of production are used and production is done at subsistence level.

- Weak industrial sector

The industrial sector is small, weak and underdeveloped due to capital constraints and poor entrepreneurial abilities.

- Underutilization of resources

Most of natural resources of the developing countries are either unutilized, underutilized or misutilized.This is due to lack of knowledge, skills, capital and market.

- High population growth rate

Demographically, low developing countries have high population growth rate due to high birth rates and declining death rates. They are associated with the problems of dependency, unemployment and balance of payment problems.

- Low life expectancy

This is due to general poor living conditions e.g. poor medical care, poor food diets e.t.c.

- Conservatism

Culturally, the behaviour of the majority is based on traditional beliefs and superstition.

The culture prohibits economic development and acceptance of new ideas. Women are generally underprivileged as they are considered inferior to man.

- Poor technology-The developing countries use backward technology with little use of scientific techniques in production.

- Low literacy level: there is abundant of unskilled labour due to high rate of illiteracy.

- High degree of independence: there is over dependence on external resources and trade.

- Shortage of entrepreneurial abilities.

- Dualism: there exist contradictory sectors i.e. traditional and modern sectors.

- Low productivity: is associated with low labour efficiency and low technology.

- Poor infrastructure: infrastructure is poorly developed i.e. poor roads, poor transports.

Factors influencing economic growth of a country

- Availability of natural resources

When natural resources are available and properly exploited then economic growth will be registered i.e. there will be an increase of the output and vice versa.

- Availability of capital stock and capital accumulation

Increased level of capital stock may result in capital widening and capital accumulation which may eventually lead to increase in level of output and vice versa.

- Technological changes

Advancement of technology significantly raises the productivity of the economy as it enables work to be done faster and leads to production of better quality of goods and services and vice versa.

- Political stability

A stable political condition is good for production to take place in an economy thus may result in increase of output. Instances of political instability however would discourage production activities to be taken.

- Increase in level of investment

Investments increase the productive capacity of an economy thus leading to high growth and vice versa.

- Government policies/interventions

If government policies are those that encourage active economic growth/production as well as promote the private sector (e.g. through reduced legal requirements, low taxes e.t.c.) the rate of economic growth is likely to be high and vice versa.

- Availability of market

When market is available and expanding i.e. both domestic and external market, the output of production will expand leading to economic growth and vice versa.

- Improvement in terms of trade

Favorable terms of trade increases the productive capacity of the economy due to high growth leading to high production and vice versa.

- Existence of good infrastructure

Existence of roads, power supply, and storage facilities e.t.c. enables production to take place leading to output increase.

- Ideal population-When the population size of a country is ideal, resource exploitation increases with increasing marginal productivity thereby leading to economic growth and vice versa.

- Industrialization

As the standard of living increases, spending on goods change from agricultural to manufactured goods. Since the opportunity for employing more capital and technology are greatest in manufacturing.

Stages of economic Growth

There are basically two attempts to classify the pattern of economic growth as passage of defining economic growth. Two stages include:

The Marx’s Classification (Karl Marx)

He saw the society as passing through the following stages:

- Primitive communism to slavery to federalism through capitalism and finally to socialism and communism.

Rostows Stages

- He views economic growth and development to take place in stages and attributed this to an analogy of an aero plane. He noted that before a plane flies off the ground, it first prepares in running in the run way, gains speed and takes off; gains altitude then stabilizes in the sky. He therefore, calls the stages of growth as: traditional, precondition to take off/transition, drive to maturity and high mass consumption.

Traditional stage

Is the stage of traditional peasant agriculture and is the first in the growth path.

Is characterized by:-

- Rudimentary methods

- Agriculture is the dominant activity

- No industrialization

- Low rate of income leading to low savings and capital accumulation.

Pre-conditional/Transitional stage

Is the stage when societies are in process of transition i.e. the period when the society lays foundation for take off.

Characteristics

- The society starts to get influenced by external forces.

- The idea of the economy progress spreads.

- Education starts spreading.

- Society starts to imitate the advanced ideas.

- Banks and other financial institutions start appearing for savings.

- Commerce and external trade widens.

- Transformation of people’s beliefs.

- Modest investment in manufacturing and communication begins to take place.

Take off stage

Involves a severe historical transformation in society where social, economic and political transformations are experienced in the economy. Is the stage when the obstacles to steady growth are removed leading to reduction of foreign dependence. The forces of the economic progress from the modern economic activities expand and dominate the society.

Characteristics

- Elimination of all obstacles of economic growth e.g. high population, growth rate, traditional cultural beliefs.

- Savings and investment increases

- Industries and market expands.

- New techniques in production are introduced in all sectors.

- One or more leading sectors of the economy emerge.

- The economy exploits formerly unused natural resources.

- Expansion of labour service and many goods are produced thus increases the availability of consumers’ choice.

- Increased urbanization and monetization.

Drive to maturity stage

Is a relatively more advanced stage than the take off stage. Is a period of long sustained economic growth where modern technology is extended to all economic activities.

Characteristics

- New production techniques replace old ones.

- High level of research and discovery.

- New leading sectors are created.

- Savings are so high.

- Development of many industries.

- Labour and other factors of efficiency are advanced hence high productivity.

- Import substitution strategy i.e. goods formerly imported are produced at home.

- Low population growth rate.

- Employment opportunities increase.

- Increased level of secondary urbanization.

- High level of infrastructure development.

High mass consumption stage

Is a stage of high consumption of goods and services. The leading industries of the economy shift from producing mainly capital goods to consumer goods. The resources are fully developed.

Characteristics

- Income of majority rise beyond subsistence

- Savings level is very high.

- Labour is highly skilled and expensive.

- Social welfare and security schemes are emphasized as the society progresses to welfare state.

Criticism of Rostows Theory

- The growth theory postulated by Rostows is not a developed strategy but merely a description of growth and development process which simply indicates that the process of economic growth is evolutionary and gradual.

- Though Rostows developed stages to elaborate accelerated growth, it is difficult to demarcate one stage from the other stage of growth i.e. there is a considerable overlapping between the different stages.

- Explains the growth in terms of savings however savings are not the only source of economic growth but other factors such as political stability etc also contribute to economic growth.

- Some countries have achieved high savings (say 5-10%) but have never taken off.

Theories of Economic Growth

Economists have put forward theories which can be used to promote economic growth. These include:-

- Balanced Growth theory

It was formulated by Ragnar Narks in his article (the problem of capital formation in under developed countries).The strategy goes for simultaneous investments in several industries, projects or sectors which will compliment each other so that where one industry alone would not be viable because of small market, the large number of industries/sectors can help to support each other. It is believed that because of the vicious cycle of poverty, there may be insufficient demand to support one industry but if many new industries are set up, income may be raised and demand increases sufficiently to support the product on industry and other industries. Different industries might also supply each other with raw materials or generate other kinds of external economies. The theory therefore, suggests simultaneous investment in large number of mutually supportive industries/sectors so that there is an equilibrium expansion and development of all sectors/industries.

Criticism of Balanced Growth theory with respect to Developing countries

- The idea of mutually supporting industries providing market for others is self- defeating since it calls for establishment of a vast number of projects simultaneously which may not be possible.

- Since projects in low developing countries face high degree of uncertainty placing high stake of minimum critical efforts implies very heavy loss incase of failure of projects.

- Shortage of skills, trained manpower and entrepreneurial activities limit the efficient application of balanced theory.

- Low developing countries have limited capital and resources to sustain balanced growth.

- Balanced growth implies over reliance on foreign aid with associated problems in debt servicing.

- Unbalanced Theory

- Proposed by Professor Albert Hirschman who said that since typical developing countries face shortage of capital, managerial abilities and entrepreneurial abilities, the resources available should be invested in all industries/sectors which have maximum effects on the economy through linkages with other potential sectors/industries.

- Such key industries/sectors which have got the highest number of forward and backward linkages are referred to as leading industries/sectors. Thus the unbalanced theory asserts that instead of investments being made on abroad front as in the case of balanced theory, it should be focused on the growing point of the leading sectors which are vital and can ultimately lead to the growth of other sectors.

- Unbalanced Theory

Criticism of Unbalanced Growth theory

- It does not offer solutions to the problems of vicious cycle of poverty in small market.

- It advocates for specialization which involves risks. Concentrating on one product/a small number of products can make the country suffer cyclical fluctuations in the world demand and supply e.g. if the taste of a commodity changes, the commodity would eventually loose its demand in market.

- May trigger inflationary problem due to inadequate/shortage in aggregate supply.

- Big push theory

It was formulated by Paul Rodeisten and calls for a comprehensive program that enables an economy to overcome problems of under development. It assigns capital, central role in the process of economic growth and development. According to the theory there should be a minimum level of resources that must be devoted to development programs for economic progress. It therefore calls for a sudden sharp increase in the rate of investment so as to achieve economic progress.

Criticisms of Big push Theory

- Neglects the economy from investing in exports industry and import substitution

- Ignores investment in agricultural sectors which is the dominant sector in low developing countries.

- Generates inflationary pressure arising from the fluctuations of prices in the economy.

- Low developing countries lack capital to launch a high minimum amount investment of social overhead which is very expensive.

Strategies for economic growth and development

- Industrialization strategy – this aims at creation of industries in the economy for production of goods and services i.e. expansion of the industrial sector.

- Population control policies – aim at ensuring an ideal population size that enables optimum resources exploitation thereby increasing productivity.

- Technological advancement – refers to the movement of technology from one country to another especially from most developed countries to the least developed ones. It facilitates the exploitation of resources increasing productivity and production of new and better quality products.