4.1 Introduction

Materials held by the organization in its stores or otherwise constitute its stock. In the ideal would stockholding would not be necessary. Demand and supply would be synchronized and materials would flow o the point of use at a rate matching the speed of consumption. This is however not the case in the real world

4.2 Reasons for Holding Stock

- Delivery cannot be exactly matched with usage day by day

- Economies associates with buying or manufacturing in large quantities more than offset the cost of storage

- Operational risks require the holding of stock to guard against breakdown on programme changes

- For work in progress where a completely balanced production flow is impracticable

- For finished goods where the holding of a buffer stock between production and the customer is desirable

- Owing to fluctuations is the price of a commodity it is desirable to acquire stocks when prices are low.

- In order that materials may appreciate in value through storage e.g. wine, coffee etc.

- In order that customers may be attracted by a range of products from which to select.

The weight given to each of these factors depends upon the type of organization and the approach to stock control will naturally be influenced by the nature of the firm’s activity. In order to adequately maintain its stock a firm must maintain stock records.

Role played by Stock Records

- To indicate the amount of stock of any item at any time without it being necessary for the stock to be counted physically.

- To establish a link between the physical stock and the stores accounts. All receipts and issues of stock cause adjustments to the stores accounts

- To provide a means of provisioning i.e. determining how much should be ordered to maintain stock at the required level.

- To supply information for stock taking, i.e matching records with physical stocks for control.

- to provide a method of informing stores staff of the location of goods in the stores

- to serve the purpose of a price list where unit prices are recorded

Definition of Inventories/Stocks

- Production inventories- raw materials, parts and components which enter the firm’s product in the production process.

- MRO inventories- maintenance repair and operating supplies which are used in the production process but which do not become part of the product e.g. lubricants

- In-process inventories- semi finished products found at various stages of the production operation

- Finished goods inventories- completed goods ready for shipment.

Stock/Inventory Analysis

This is the process of determination and classification of all that is held in stock by the firm. Sound inventory management requires the development of a complete inventory catalogue followed by a thorough ABC analysis

Inventory Catalog

An inventory catalog is some form of classification of inventory items in some type of categories the most common category is the function of the items. For an inventory catalog to be prepared all inventory items have to be completely described , identified by the manufacturers part number and cross- indexed by users identification number if necessary. Inventory catalogs are very useful in:

- Serving a medium of communication by enabling staff to tell which items are carried in the inventory, whether interchangeable items are carried in the inventory for missing items. etc

- Acting as an inventory control tool through reduction of duplicate records for identified parts.

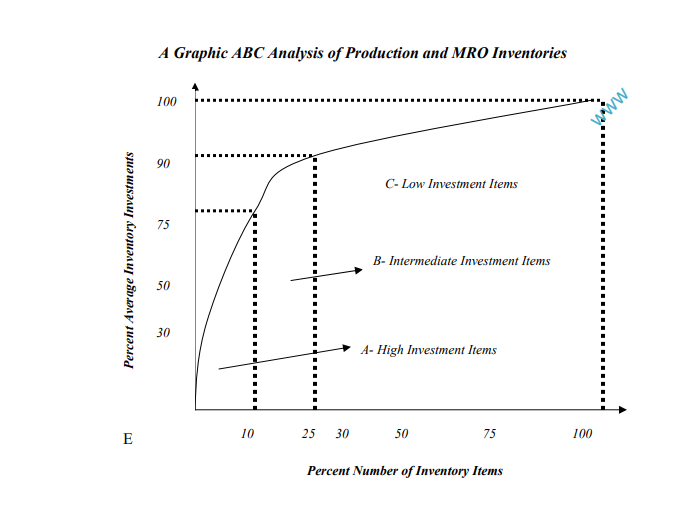

4.3 ABC Analysis: The 80-20 Concept

ABC analysis is also called Pareto analysis after Vilfredo Pareto an Italian economist who developed the concept during the early 20th century. Several studies made of large corporations have shown that 80% of all items carried in the inventory constitute 20% of the total investment while 20%of inventory items constitute 80 of total investment. In practice an ABC analysis can be made on the basis of either the average inventory investment in each item or the arrival shilling usage of each item.

Each item value is expressed as a percentage of the total inventory investment. Each item can be the fitted on the three classifications A, B, and C depending on the items percentage investments over the total inventory investment. The value of such an analysis so to provide a sound basis on which allocate time and personnel with respect to procurement management and the refinement of control over the individual inventory items. Clearly no manager wants to spent 75% of his time on class C low-value items and spend 25% of his time on class A high-value items An additional classification dependant on criticalness of each item can be added to the ABC system. This classification is on a three-point scale; 1- critical, 2 medium, 3 non critical. Thus an item can be A1, A2, or A3 etc

Each item value is expressed as a percentage of the total inventory investment. Each item can be the fitted on the three classifications A, B, and C depending on the items percentage investments over the total inventory investment. The value of such an analysis so to provide a sound basis on which allocate time and personnel with respect to procurement management and the refinement of control over the individual inventory items. Clearly no manager wants to spent 75% of his time on class C low-value items and spend 25% of his time on class A high-value items An additional classification dependant on criticalness of each item can be added to the ABC system. This classification is on a three-point scale; 1- critical, 2 medium, 3 non critical. Thus an item can be A1, A2, or A3 etc